HMO vs. PPO vs. EPO: How to Choose the Right Health Insurance Plan

Choosing the right health insurance plan can be daunting, especially with the variety of options available. Understanding the differences between HMO, PPO, and EPO plans is crucial for making an informed decision that aligns with your healthcare needs and financial situation. This article will delve into the key distinctions among these health insurance types, helping you navigate the complexities of coverage, costs, and provider access. Many individuals and families struggle with selecting a plan that offers the right balance of affordability and flexibility. By exploring the unique features of each plan type, you can find a solution that best fits your lifestyle. We will cover the differences among coverage options, the best plans for families and small businesses, and how to use comparison tools effectively to make your choice.

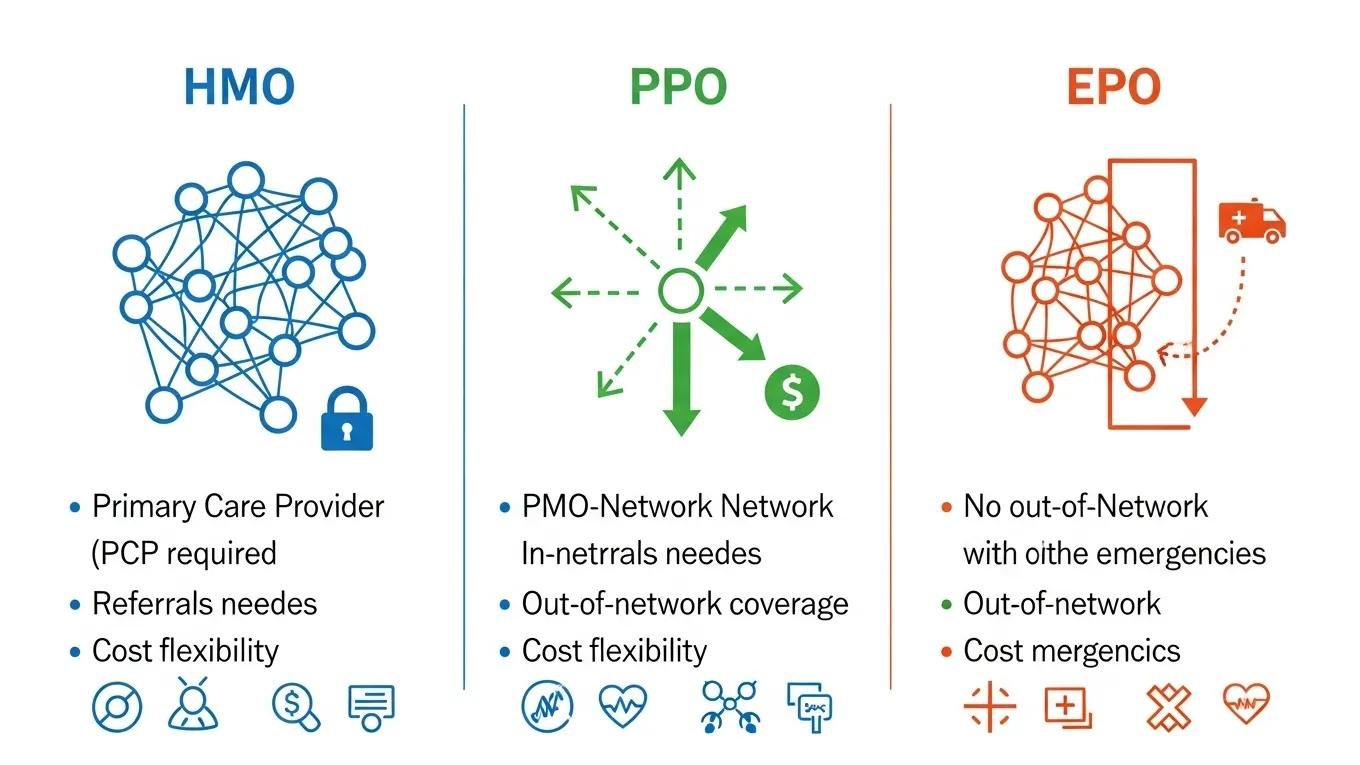

What Are the Key Differences Between HMO, PPO, and EPO Health Insurance Plans?

HMO, PPO, and EPO plans each offer distinct features that cater to different healthcare needs. An HMO (Health Maintenance Organization) plan typically requires members to choose a primary care physician (PCP) and obtain referrals for specialist services. This structure often results in lower premiums and out-of-pocket costs, making it an attractive option for those seeking affordable healthcare. In contrast, PPO (Preferred Provider Organization) plans provide greater flexibility, allowing members to see any healthcare provider without a referral, including specialists. However, this flexibility often comes with higher premiums and out-of-pocket expenses. EPO (Exclusive Provider Organization) plans combine elements of both HMO and PPO plans, offering a network of providers without requiring referrals, but they do not cover any out-of-network care except in emergencies.

The unique structure of EPO plans, often seen as a hybrid, provides a distinct balance between the strictness of HMOs and the flexibility of PPOs regarding out-of-network care.

EPO vs. PPO vs. HMO: Understanding Out-of-Network Benefits

(EPO) is essentially a PPO with no out-of-network benefit. Although similar to an HMO in that respect, the EPO does This feature makes an EPO more attractive than an HMO to some

Managed care organizations and products, 1997

Understanding these differences is essential for selecting the right plan that meets your healthcare needs while considering your budget.

Which Health Insurance Plan Is Best for Families and Small Businesses?

When evaluating health insurance options for families and small businesses, several factors come into play, including coverage needs, flexibility, and cost-effectiveness. Families often benefit from HMO plans due to their focus on preventive care and lower overall costs. These plans typically cover essential health services, including routine check-ups and vaccinations, which are crucial for maintaining family health. Small business owners, on the other hand, may prefer PPO plans for their flexibility, allowing employees to access a broader range of specialists without needing referrals.

What Benefits Do HMO Plans Offer for Family Coverage?

HMO plans provide several advantages for family coverage, primarily through their emphasis on preventive care. Families can enjoy lower premiums and out-of-pocket costs, making healthcare more accessible. Additionally, HMO plans often include comprehensive wellness programs that encourage regular check-ups and screenings, which can lead to early detection of health issues. Coordinated care through a primary care physician ensures that families receive consistent and comprehensive health management.

How Do PPO Plans Provide Flexibility for Small Business Owners?

PPO plans are particularly beneficial for small business owners who require flexibility in their healthcare options. These plans allow employees to choose their healthcare providers without needing referrals, which can be crucial for accessing specialized care quickly. Furthermore, PPO plans often include out-of-network coverage, allowing employees to seek care from a wider range of providers. This flexibility can enhance employee satisfaction and retention, making PPO plans an attractive option for small businesses.

How Does the Enrollment Process Differ for HMO, PPO, and EPO Plans?

The enrollment process for HMO, PPO, and EPO plans varies significantly, impacting how individuals and families can access healthcare. HMO plans typically require members to select a primary care physician during enrollment, which can streamline the process of obtaining specialist referrals. In contrast, PPO and EPO plans allow for more straightforward enrollment, as members do not need to choose a PCP or obtain referrals. This difference can make PPO and EPO plans more appealing for those who prefer immediate access to specialists without additional steps.

Comparing HMO, PPO & EPO Health Plans: Key Differences

Each health insurance plan type comes with its own set of advantages and limitations. HMO plans are cost-effective and emphasize preventive care, but they may limit provider choice and require referrals. PPO plans offer greater flexibility and access to a wider network of providers, but they come with higher costs. EPO plans strike a balance between the two, providing some flexibility without requiring referrals, but they do not cover out-of-network care. Understanding these pros and cons is essential for making an informed decision that aligns with your healthcare needs.

How Does Network Coverage Vary Among HMO, PPO, and EPO Plans?

Network coverage is a critical factor when choosing a health insurance plan. HMO plans require members to use a network of providers, and out-of-network care is generally not covered except in emergencies. PPO plans, however, offer a more extensive network and allow members to seek care from out-of-network providers, albeit at a higher cost. EPO plans provide a network of providers similar to HMOs but do not require referrals, making them a middle ground between HMO and PPO plans. Understanding these network differences can help you choose a plan that ensures access to your preferred healthcare providers.

State regulations often play a significant role in defining and expanding network adequacy requirements across different plan types.

State Policies on HMO, PPO, & EPO Network Adequacy

New York expanded its network adequacy policies, which previously applied only to HMOs, to include PPO and EPO plan types. Additionally, New York implemented the arbitration of

Impact of Out-Of-Network Service Utilization and State Policy Changes on Payments and Follow-Up Visits, 2019

What Are the Cost Structures and Out-of-Pocket Expenses for Each Plan Type?

Cost structures and out-of-pocket expenses vary significantly among HMO, PPO, and EPO plans. HMO plans typically feature lower premiums and out-of-pocket costs, making them an economical choice for families. PPO plans, while offering greater flexibility, usually have higher premiums and deductibles, leading to higher out-of-pocket expenses. EPO plans offer moderate premiums and out-of-pocket costs, providing a balance between affordability and flexibility. Evaluating these cost structures is essential for selecting a plan that fits your budget while meeting your healthcare needs.

How Can Bilingual Support Enhance Your Insurance Enrollment Experience?

Bilingual support can significantly enhance the insurance enrollment experience for diverse clients. Many individuals face language barriers that can complicate their understanding of health insurance options. By providing bilingual assistance, insurance providers can ensure that clients fully comprehend their choices, benefits, and the enrollment process. This support not only improves client satisfaction but also fosters a more inclusive environment, allowing individuals from various backgrounds to make informed decisions about their health insurance.

How Can You Use Comparison Tools to Choose the Right Health Insurance Plan?

Using comparison tools can simplify the process of selecting the right health insurance plan. These tools allow individuals to evaluate different plans side by side, highlighting key features such as premiums, coverage options, and provider networks. When using comparison tools, it is essential to consider personal healthcare needs and financial situations to make an informed choice. Additionally, many comparison tools provide user-friendly interfaces that make it easy to navigate complex information, ensuring that users can find the best plan for their needs.

What Features Should You Look for in an Insurance Quote Widget?

When evaluating insurance quote widgets, several features can enhance the user experience and facilitate informed decision-making. Key features to look for include:

- Comparison Capabilities: The ability to compare multiple plans side by side.

- User Interface Considerations: An intuitive design that simplifies navigation and information retrieval.

- Real-Time Updates: Access to the latest information on plan availability and pricing.

These features can significantly improve the process of obtaining and comparing health insurance quotes, making it easier for individuals to find the right plan.

How Do Comparison Tables Help Clarify Plan Differences?

Comparison tables are valuable tools for understanding the differences among health insurance plans. By presenting information in a clear and organized format, these tables allow users to quickly identify key features, such as coverage options, costs, and provider networks. This visual representation simplifies complex information, enabling individuals to make informed decisions about their health insurance choices. Using comparison tables can enhance the decision-making process, ensuring users select a plan that best meets their needs.

What Are Common Questions About HMO, PPO, and EPO Plans?

Many individuals have common questions regarding HMO, PPO, and EPO plans. Addressing these questions can help clarify misconceptions and provide valuable insights into each plan type. Some frequently asked questions include:

- What is the primary difference between HMO and PPO plans? HMO plans require referrals and have lower costs, while PPO plans offer more flexibility and higher costs.

- Can I see a specialist without a referral in an HMO plan? No, HMO plans typically require a referral from a primary care physician to see a specialist.

- Are EPO plans a good option for those who want flexibility? Yes, EPO plans offer flexibility without requiring referrals, but they do not cover out-of-network care.

By addressing these common questions, individuals can gain a better understanding of their health insurance options and make informed decisions.

Are PPO Plans More Expensive Than HMOs?

PPO plans are generally more expensive than HMO plans due to their increased flexibility and broader provider networks. While HMO plans offer lower premiums and out-of-pocket costs, PPO plans allow members to see any provider without a referral, including out-of-network options. This flexibility comes at a price, making PPO plans a more costly choice for individuals and families. Understanding these cost differences is essential for selecting a health insurance plan that aligns with your budget and healthcare needs.

Frequently Asked Questions

What should I consider when choosing between HMO, PPO, and EPO plans?

When selecting between HMO, PPO, and EPO plans, consider factors such as your healthcare needs, budget, and preferred level of flexibility. Evaluate the cost structures, including premiums and out-of-pocket expenses, as well as the available provider network. If you prioritize lower costs and preventive care, an HMO may be suitable. For those who value flexibility and access to specialists without referrals, a PPO might be the best choice. EPOs offer a middle ground, so assess which features align with your lifestyle.

How do I know if I need out-of-network coverage?

Determining the need for out-of-network coverage depends on your healthcare preferences and provider relationships. If you have established relationships with specific specialists or prefer a wider range of healthcare options, a PPO plan may be beneficial due to its out-of-network coverage. Conversely, if you are comfortable using in-network providers and prioritize cost savings, an HMO or EPO plan may suffice. Assess your current healthcare needs and future expectations to make an informed decision.

Can I switch health insurance plans during the year?

Switching health insurance plans outside the open enrollment period is generally limited to qualifying life events, such as marriage, the birth of a child, or the loss of other coverage. If you experience such an event, you may be eligible for a special enrollment period, allowing you to choose a new plan. However, if you are satisfied with your current plan and do not anticipate significant changes, it may be best to wait until the next open enrollment period to make adjustments.

What are the implications of choosing a plan with a high deductible?

Choosing a health insurance plan with a high deductible can lead to lower monthly premiums, but it also means you will pay more out-of-pocket before your insurance coverage kicks in. This can be beneficial for those who are generally healthy and do not anticipate frequent medical visits. However, if you require regular care or have ongoing health issues, a high deductible can lead to higher costs. Carefully evaluate your healthcare needs and financial situation before selecting a plan with a high deductible.

How can I find the best health insurance plan for my specific needs?

To find the best health insurance plan for your needs, start by assessing your healthcare requirements, including any ongoing treatments or medications. Use comparison tools to evaluate different plans based on coverage options, costs, and provider networks. Additionally, consider seeking advice from insurance brokers or utilizing resources from healthcare marketplaces. Gathering information and understanding your priorities will empower you to make an informed decision that aligns with your health and financial goals.

What role does preventive care play in health insurance plans?

Preventive care is a crucial component of many health insurance plans, particularly HMOs. It includes services such as routine check-ups, vaccinations, and screenings aimed at preventing illnesses before they develop. Many plans cover these services at no additional cost to encourage members to prioritize their health. Understanding the preventive care benefits of your chosen plan can help you maintain your well-being and potentially reduce long-term healthcare costs by catching issues early.

Conclusion

Choosing the right health insurance plan—whether HMO, PPO, or EPO—can significantly impact your healthcare experience and financial well-being. Each plan type offers unique benefits, from the cost-effectiveness of HMOs to the flexibility of PPOs, ensuring that you can find a solution tailored to your needs. By understanding these differences, you empower yourself to make informed decisions that align with your healthcare goals. Start exploring your options today to secure the best health insurance plan for you and your family.

Written by

Kenroy Simmons

Health Insurance Expert • National Producer #18385323

Licensed, independent insurance agent at K Simmons Insurance, helping families and businesses across 32 states find the right health and life coverage.

View full profile ›

Have questions about your coverage?

Get a free, no-obligation comparison across top carriers.

☎ Call 888-984-6270