Protect Your Home with Clear, Trusted Homeowners Insurance from K Simmons Protection

Homeowners insurance is your financial safety net against the unexpected. This guide walks through the core parts of a homeowner’s policy—what it covers, what drives your premium, and how to pick the right plan for your needs. With clear explanations and local insight from K Simmons Protection, you’ll know how to protect your home, belongings, and peace of mind. We’ll cover common types of coverage, how claims work, discounts to look for, and the advantages of our bilingual service.

What homeowners' insurance coverages should you know about?

Homeowners policies bundle several protections that work together to safeguard your house and everything inside it. According to the Insurance Information Institute, standard policies typically include dwelling coverage, personal property coverage, liability protection, and coverage for additional living expenses if your home becomes unlivable.

Dwelling coverage: rebuilding or repairing your home

Dwelling coverage helps pay to repair or rebuild the physical structure of your home after covered events like fire, wind damage, or vandalism. It typically covers the main house, attached structures such as garages, and, in some policies, certain landscaping or built-in features. Make sure your dwelling limit reflects the cost to rebuild—not just the market value—so you aren’t left underinsured after a loss.

Personal property and liability coverage made simple

Personal property coverage replaces or repairs items inside your home—furniture, electronics, clothing—if they’re stolen or damaged by covered causes. Liability coverage helps if someone is hurt on your property or you’re legally responsible for damage to another person’s belongings. Together, these coverages help protect you from unexpected bills and legal claims.

How are home insurance rates set and what affects your premium?

Knowing what insurers consider when setting rates can help you make choices that control costs. The National Association of Insurance Commissioners (NAIC) outlines many of the common factors insurers use when pricing policies.

Key factors that influence home insurance costs

Your premium depends on factors such as your home’s location, replacement cost, claims history, and the limits you choose. Houses in areas with a higher risk of storms, floods, or theft usually cost more to insure. The home’s age and condition also matter—older homes or homes with outdated wiring or roofing can increase premiums. In Florida, hurricane and flood exposure are major rate drivers.

Practical ways to lower your home insurance premium

You can often reduce premiums by increasing your deductible, bundling multiple policies (home and auto), improving home security, and keeping a clean claims record. Shopping around and comparing offers from licensed local agents can also uncover better pricing. Good credit and routine home maintenance are additional steps that often lead to savings.

Strategies for Reducing Home Insurance Premiums

Simple, proven steps can lower premiums across auto, home, and health insurance—Many savings come from raising deductibles, bundling policies, and improving home security.

How to save hundreds on insurance with these simple hacks, M Celestin, 2022

What should you consider when choosing the best homeowners policy?

Picking the right policy means weighing coverage limits, deductibles, exclusions, and the insurer’s reputation. The Florida Department of Financial Services has tools to help consumers compare policies and understand common terms.

Review policy features and deductible choices

Look closely at coverage caps for personal items, whether replacement cost or actual cash value applies, and any separate limits for valuables like jewelry. Choose deductibles that balance affordable monthly premiums with an amount you can pay out of pocket after a loss. Clear, readable policy documents make it easier to compare options and spot gaps.

Greater transparency in how policies are written and presented helps homeowners make better decisions—especially when coverage details affect out-of-pocket costs after a claim.

Improving Homeowners Insurance Coverage Transparency

Experts recommend making full policy texts and clear summaries publicly available so consumers can compare coverages and exclusions more easily.

Improving the Market for Homeowners Insurance, 2023

How K Simmons Protection’s personalized consultations help

At K Simmons Protection, we sit down with you—in person or over the phone—to map your risks, review limits, and recommend the right mix of coverages. Personalized guidance helps you avoid surprises and choose policy features that match your home and budget. As the Consumer Financial Protection Bureau points out, one-on-one advice is often the quickest way to make confident insurance choices.

Protecting your home and lifestyle in Bradenton

Bradenton is a place people love for its waterfront, parks, and tight-knit neighborhoods. Homeowners insurance here protects more than a building—it protects the ways you live, celebrate, and relax. Local landmarks like the Bradenton Riverwalk and community events help define life in the area, and reliable coverage preserves that lifestyle when the unexpected happens.

Places like the South Florida Museum and the De Soto National Memorial are part of Bradenton’s identity. K Simmons Protection understands these local ties and offers insurance designed for the region’s needs.

The annual Manatee County Fair and other community traditions remind us why good coverage matters: to protect homes, memories, and neighborhood connections. We’re committed to helping Bradenton homeowners keep that protection in place.

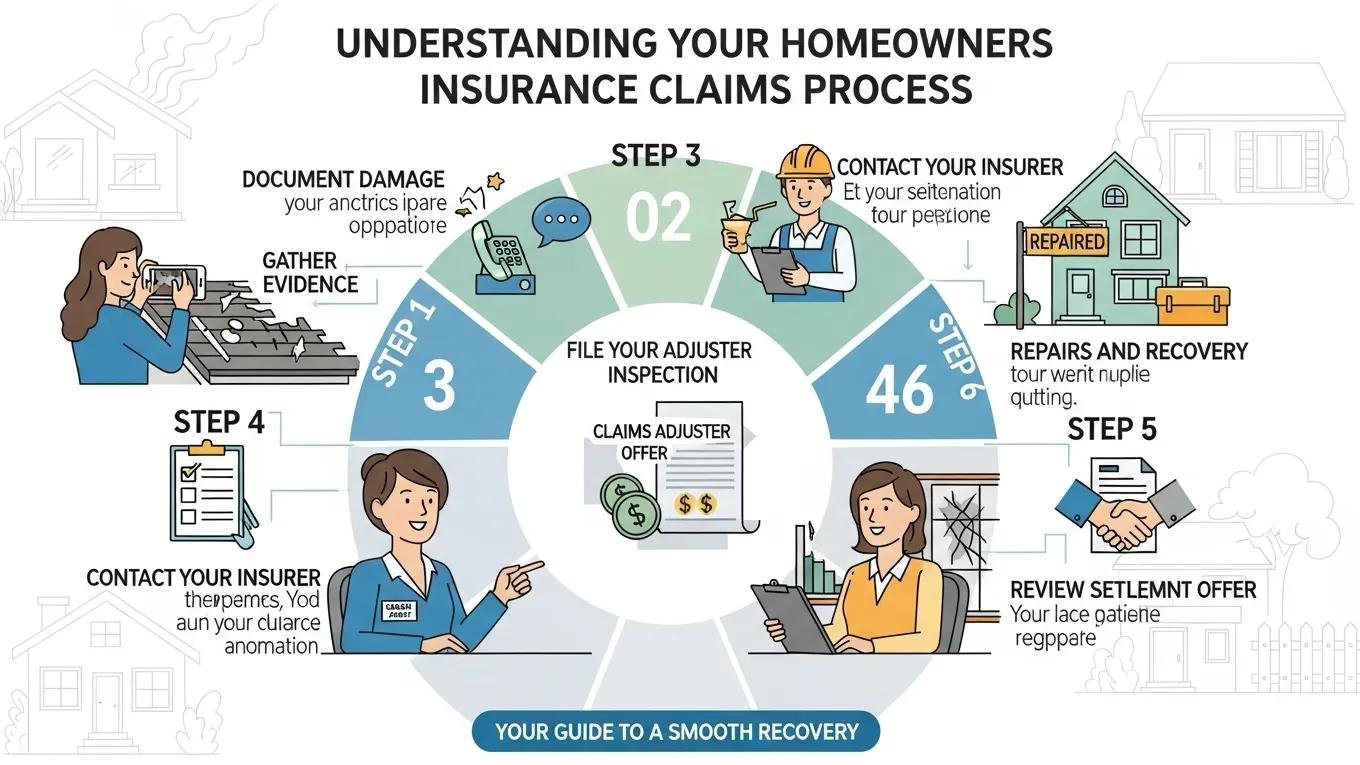

How does the homeowners' insurance claims process work?

Knowing the steps in a claim helps you act quickly and get a fair outcome.

Step-by-step: filing a home insurance claim

Start by reporting the loss to your insurer and provide basic details. Document damage with photos and a written inventory. Your insurer will assign an adjuster, who may visit to inspect the damage and review repair estimates. Keep receipts for temporary repairs and any living expenses if you’re displaced. Being organized and responsive speeds up the process.

Tips for a smoother claims experience

Keep clear records, take lots of photos, and keep copies of all communications. Notify your agent early, and ask questions if you don’t understand a step. If something seems off, request clarification in writing. Staying calm, thorough, and communicative is the best way to protect your claim.

What discounts and savings does K Simmons offer?

K Simmons Protection helps homeowners find discounts that lower premiums without sacrificing needed coverage.

Common homeowners insurance discounts

Discounts often include savings for bundling home and auto policies, installing alarm systems, maintaining a claims-free record, or making storm-resistant upgrades. Ask your agent about discounts that apply to your home—small upgrades can add up to meaningful savings.

Save more with bundled financial and credit-repair services

We also offer bundled services—such as basic financial planning and credit repair assistance—that can make insurance more affordable over time. Combining services with your insurance can help improve rates and simplify your financial planning.

How do bilingual services improve your insurance experience?

Access to service in your preferred language makes a real difference during quotes, policy explanations, and claims.

Why bilingual support matters

Bilingual agents help clients understand policy details, ask the right questions, and feel confident about coverage choices. Clear communication reduces mistakes and builds trust, especially for clients who prefer to speak in their native language.

Get personalized consultations in the language you prefer

K Simmons Protection provides consultations in multiple languages so you can discuss concerns comfortably and get advice that fits your needs. That personal touch ensures you leave a meeting feeling informed and confident about your coverage.

Frequently Asked Questions

What should I do if I experience a natural disaster in my area?

Your family’s safety comes first. After you’re safe, photograph and document all damage, keep receipts for emergency repairs, and contact your insurance provider immediately to report the loss. Your insurer will explain the next steps, including inspections and temporary housing help if needed. Keep a log of all calls and correspondence to help your claim move smoothly.

How can I ensure my homeowners' insurance policy stays relevant over time?

Review your policy at least once a year and after major events—such as renovations, big purchases, or life changes. Update coverage limits to match current replacement costs and inventory values. Talk with your agent about new local risks and any discounts you may qualify for as circumstances change.

What are the benefits of working with a local insurance agent?

Local agents know regional risks, building codes, and common weather issues that affect coverage. They offer hands-on support, face-to-face meetings when needed, and faster, personalized service. That local knowledge can lead to better policy choices and more confident decisions.

Can I change my homeowners' insurance provider at any time?

Yes—you can switch providers whenever you choose. Before canceling your current policy, compare quotes and have the new policy active to avoid gaps. Check for any cancellation fees and make sure coverage limits meet your needs. Your agent can help coordinate the transition smoothly.

What is the role of an insurance adjuster in the claims process?

An adjuster investigates your claim, inspects damage, reviews your policy, and estimates repair or replacement costs. Their report influences the settlement amount. Provide them with complete documentation and be available to answer questions so the adjuster has the information needed to process your claim fairly.

How can I prepare for a homeowners insurance consultation?

Bring your current policy, a list of major belongings, recent appraisals, and notes about upgrades or repairs. Be prepared to discuss your budget and any coverage concerns. The more details you provide, the better your agent can tailor a policy to protect your home and finances.

What factors should I consider when determining the amount of coverage I need?

Consider the replacement cost of your home, the value of personal items, and any additional structures, such as sheds or detached garages. Factor in local risks—flood, hurricane, or fire—and whether you want replacement-cost or actual-cash-value coverage for belongings. An agent can help run numbers so you choose the right limits.

How can I file a claim if my home is damaged?

Report the incident to your insurer as soon as possible. Take photos, make a list of damaged items, and save receipts for emergency repairs. Your insurer will assign an adjuster and walk you through the next steps. Stay organized and keep copies of all documents related to the claim.

Are there specific discounts available for Florida homeowners' insurance?

Yes. In Florida, discounts may be available for hurricane-resistant features, bundled policies, alarm systems, and a claims-free history. Some insurers also offer savings for participating in community preparedness programs. Ask your agent which discounts apply to your property.

What should I do if my insurance claim is denied?

First, read the denial letter carefully to understand the reason. You can appeal and submit additional documentation or evidence. Talk with your agent for help and consider hiring a public adjuster or seeking legal advice if needed. Clear, documented communication increases the chance of a successful appeal.

How often should I review my homeowners' insurance policy?

Review your policy annually or after any major life or property changes—such as renovations, major purchases, or changes in occupancy. Regular reviews help ensure your coverage stays current with replacement costs and personal needs.

What is the difference between actual cash value and replacement cost coverage?

Actual cash value (ACV) pays what items are worth today after depreciation. Replacement cost covers the cost of replacing damaged items with new ones of a similar kind and quality, without deducting depreciation. Replacement cost offers stronger protection but usually carries higher premiums.

What does homeowners' insurance cover in Florida?

In Florida, standard homeowners insurance generally covers the home’s structure, personal belongings, liability, and additional living expenses if your home is uninhabitable due to a covered event.

How much does homeowners' insurance cost in Bradenton, Florida?

Premiums vary based on home value, location, coverage levels, and risk factors. A local agent like K Simmons Protection can review your situation and help find options that fit your budget.

Do I need homeowners' insurance if I own my home outright in Florida?

While not legally required if you own your home outright, insurance is strongly recommended to protect your investment from hurricanes, floods, fires, and other risks common in Florida.

Who is the best homeowners' insurance agent in Bradenton, Florida?

K Simmons Insurance provides personalized, bilingual service and complimentary consultations to help Bradenton homeowners find the right coverage for their needs.

Secure Your Home with K Simmons Protection Homeowners Insurance

Homeowners insurance is a practical way to protect your property and your peace of mind—especially here in Bradenton, where weather and local risks are part of life. Understanding coverages, comparing rates, and taking advantage of discounts help you get strong protection without surprises. K Simmons Protection offers local, personalized guidance and bilingual service to help you choose the policy that fits your home and budget. Contact us to review your options and take the next step in safeguarding what matters most.

Comprehensive Homeowners Insurance Guide by K Simmons Protection